The U.S. economy added just 199,000 net new jobs in December 2021, far below what forecasters were expecting. The unemployment rate ticked down to 3.9%, and labor force participation held steady. Wage growth continues to be strong, up 4.7% year-over-year. This report does not fully reflect the surge of Omicron cases, however. What does it mean for recruiters? Workers who want a job are getting them, but employer demand is slowing a bit from the frenetic pace of job gains earlier in 2021. And meanwhile the labor force has not surged back to pre-pandemic levels. It’s a workers’ market and recruiting is still hard.

Pre-Omicron hiring slowed, a worrisome sign

The labor market is still at the mercy of the virus. The reference week of these December numbers came mid-month, before the surge of COVID cases from the Omicron variant. Forecasters had projected around 400,000 net new jobs, so 199,000 is a disappointment. But this is the pre-Omicron hiring trend, and November job growth was also weaker-than-expected (249,000).

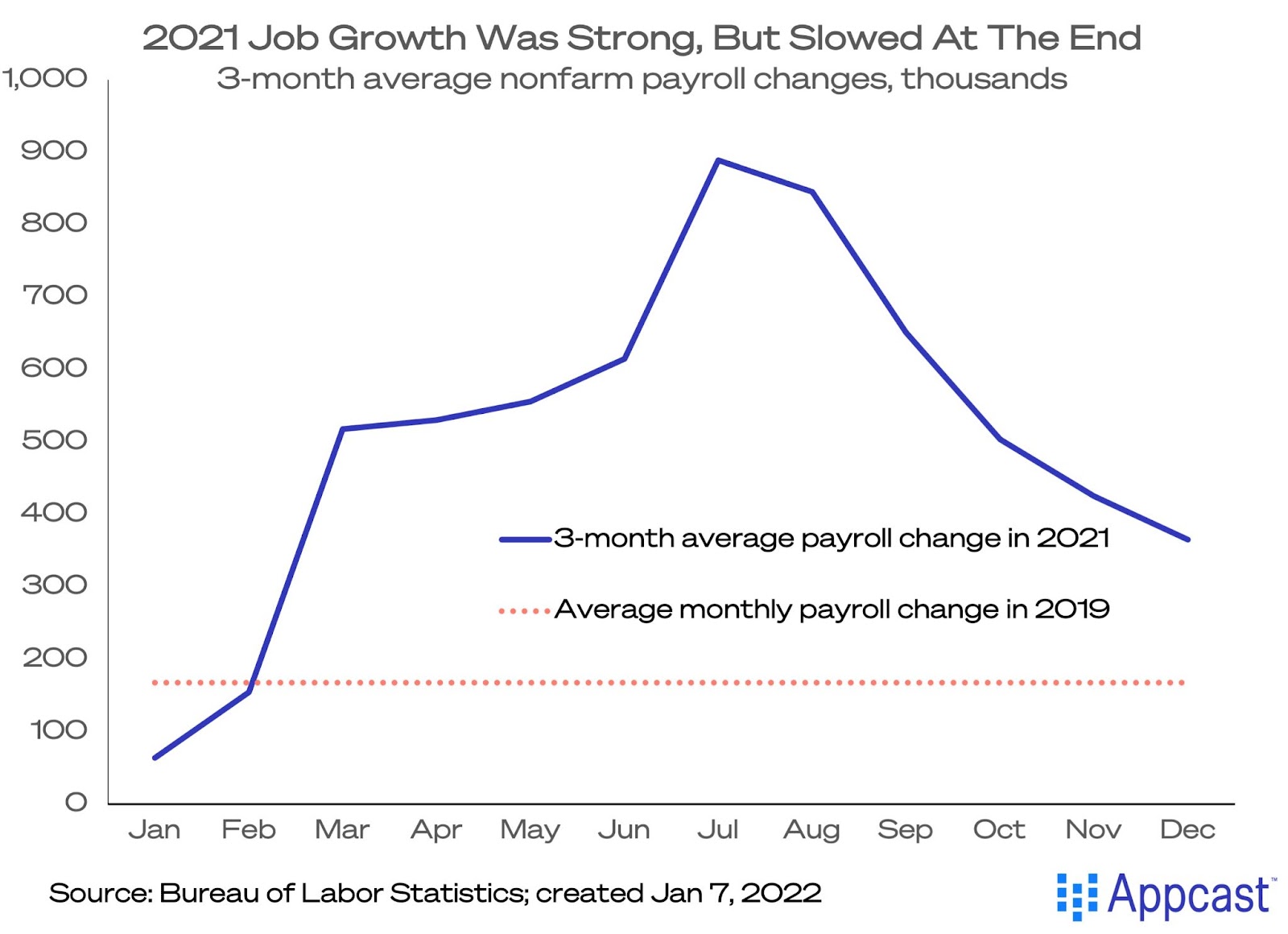

For the entire year 2021, job growth was strong overall – much higher than the average monthly gain in 2019, pre-pandemic. That year payroll job growth averaged 168,000 per month, but in 2021 the average was 537,000. The three-month moving average in 2021 shows how job growth accelerated in the spring and summer, as vaccines became widely available, with payroll gains peaking mid-year. Then hiring growth slowed as COVID variants emerged.

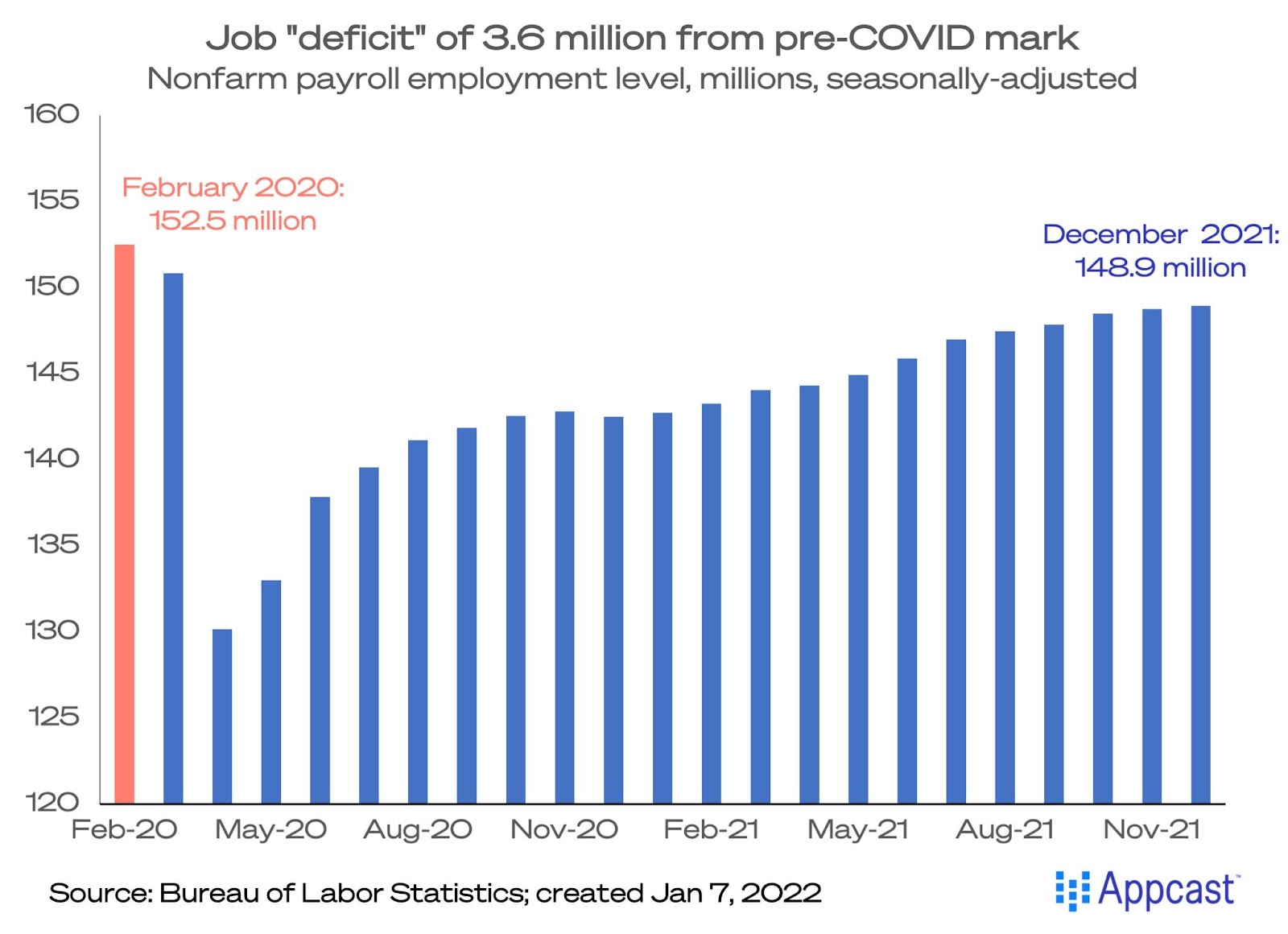

There is still a lot of catching up to do. While the US economy added 6.5 million jobs in 2021, the job “deficit” compared to pre-pandemic times is 3.6 million, or 2.3% below February 2020 levels.

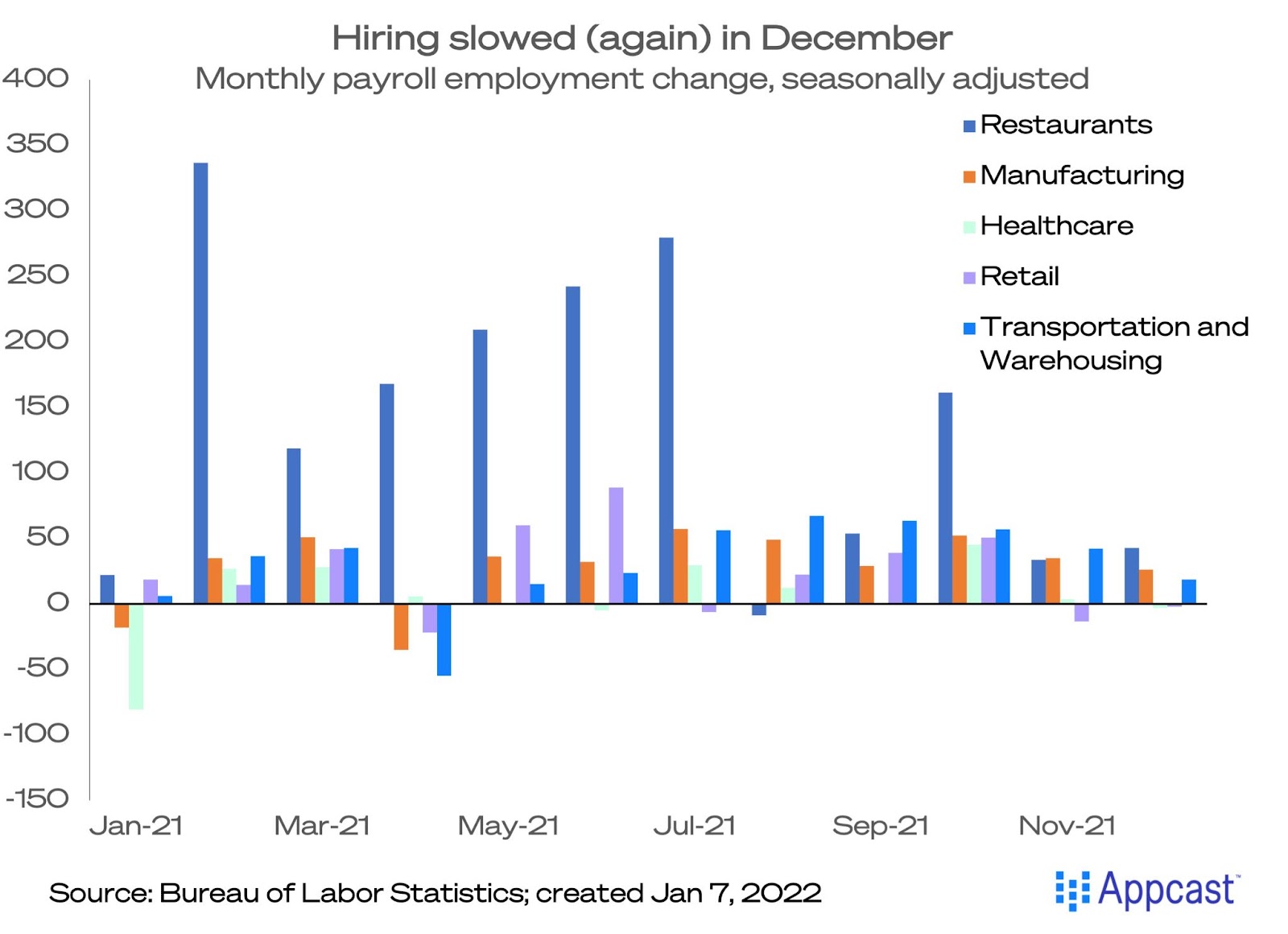

Hiring slowed across most industries in December

The industry-level breakdowns were disappointing. Restaurant jobs grew by 43,000, which is great in most years; but as recently as October this industry was seeing job gains above 160,000. Retail jobs shrunk by 2,000. Transportation and Warehousing, normally a bright spot in 2021, saw jobs grow by a lackluster 19,000. Healthcare payrolls declined by 3,000 and Manufacturing rose by 26,000.

Data from individuals (aka the household survey) showed employment growth of 651,000 on the month, a conflicting signal from the payroll (employer) survey. Seasonal adjustments and revisions to past month’s data have been wacky in 2021, as the pandemic has distorted typical hiring patterns.

Labor force is rebounding to pre-pandemic levels, albeit slowly

According to the household survey, the unemployment rate ticked down sharply, by 0.3 percentage points, to 3.9%. The total labor force grew by nearly 168,000, a lot less than in November. So the labor force participation rate was flat at 61.9%, and the employment to population ratio rose just slightly, to 59.5%.

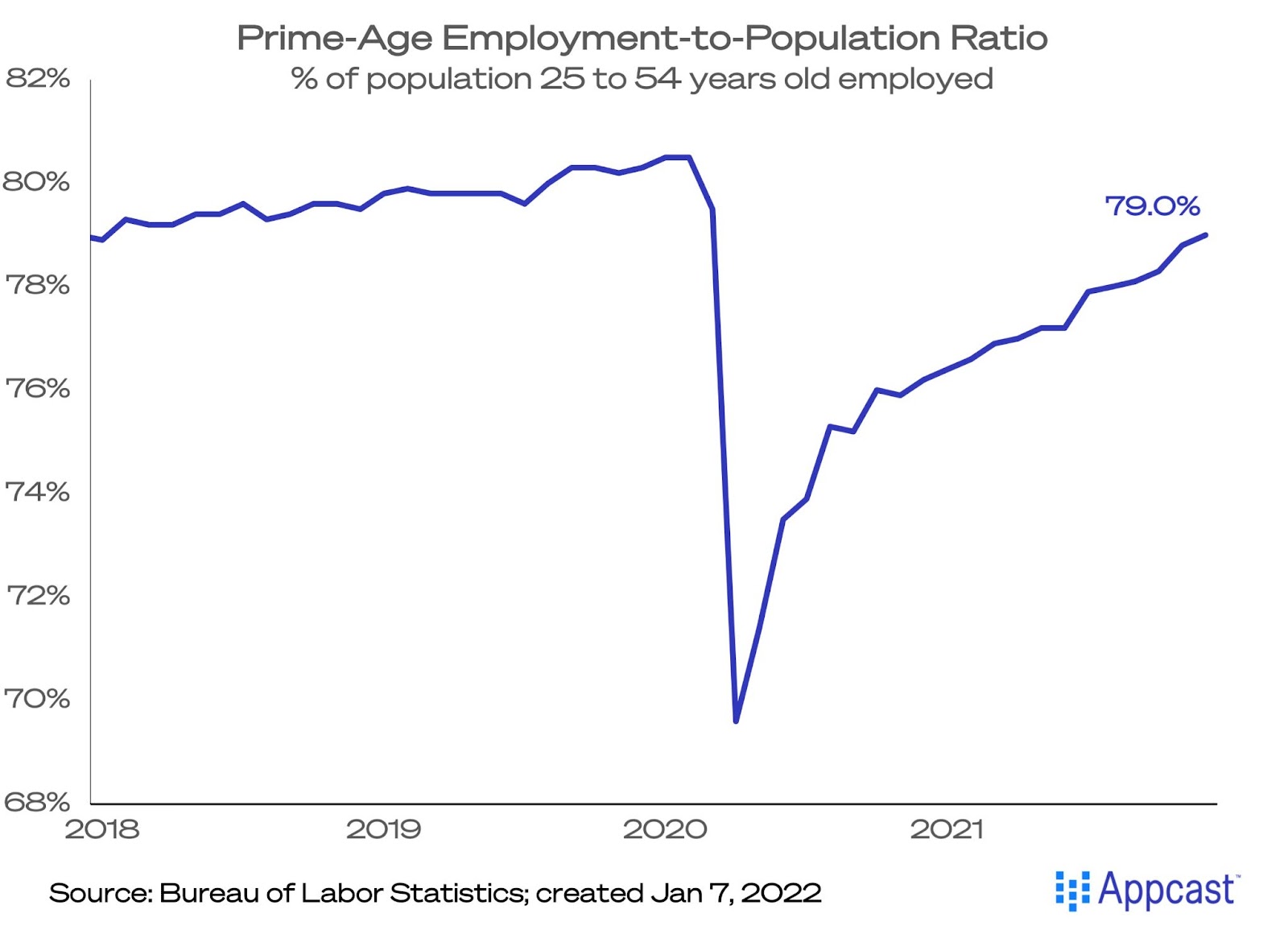

The best metric for labor supply – the prime-age employment to population ratio – rose two-tenths, to 79.0%. All around, the household survey showed a decent rebound in worker participation. People who want a job are finding plenty of openings available. But a lot of folks are still on the sidelines: 5.6 million people want a job but aren’t actively looking. The labor force has not fully rebounded to pre-pandemic levels.

Wage growth continues to be strong, but so does inflation

Wage gains continue to accelerate, but will it outpace inflation? Average hourly earnings growth continues to be strong, up 4.7% year-over-year. But as we all know, these are nominal gains (not adjusted for inflation). Employers are eager to hire – reflected in the 10.6 million job openings in November. However, given that many would-be job seekers remain skittish about joining the labor force, this has resulted is labor shortages in some industry and thus strong wage gains to entice prospective workers

Average hourly earnings for rank-and-file workers – production and nonsupervisory employees – were up 5.8% year-over-year. From February 2020, nominal wages are 11.1% higher for rank-and-file employees, and up 9.8% for all workers. Despite the strong nominal wage growth, for many workers bigger paychecks may not outpace inflation, which is at a 40-year high.

What does this mean for recruiters?

Weaker-than-expected job growth (according to the establishment survey) conflicts with decent increases in labor force participation (according to the household survey). If more would-be job seekers are lured into the labor force from rising wages, that could ease recruiting challenges. That said, with record-shattering levels of jobs available, this tight labor market does not appear to be going away anytime soon.

Could the Omicron variant dampen hiring demand in January? For sure, as these numbers are based on surveys taken before the surge of COVID cases in late December. While this jobs report was a bit of a disappointment, the overall story of the labor market in 2021 remains the same: competition for workers is intense.